Existing-home sales are projected to climb by 14% in 2026, marking a decisive break from the stagnation that defined the previous three years. This recovery is underpinned by a dual-engine effect: a measurable increase in housing inventory and a stabilizing interest rate environment guided by the Federal Open Market Committee's June 2026 projections. For buyers and sellers who have been "waiting out" the market, the mid-year data suggests that the window of peak inactivity has closed, replaced by a period of selective opportunity where regional affordability remains the primary hurdle.

Why is the 2026 housing market expanding?

The 2026 market expansion is driven by a massive release of pent-up demand as lower mortgage rates and rising supply finally align. After years of homeowners being "locked-in" to low pandemic-era rates, a critical mass of sellers has begun to list properties, providing the inventory necessary to support higher transaction volumes. National Association of REALTORS® Chief Economist Lawrence Yun notes that this year represents the first measurable increase in sales after a prolonged period of high-interest hovering.

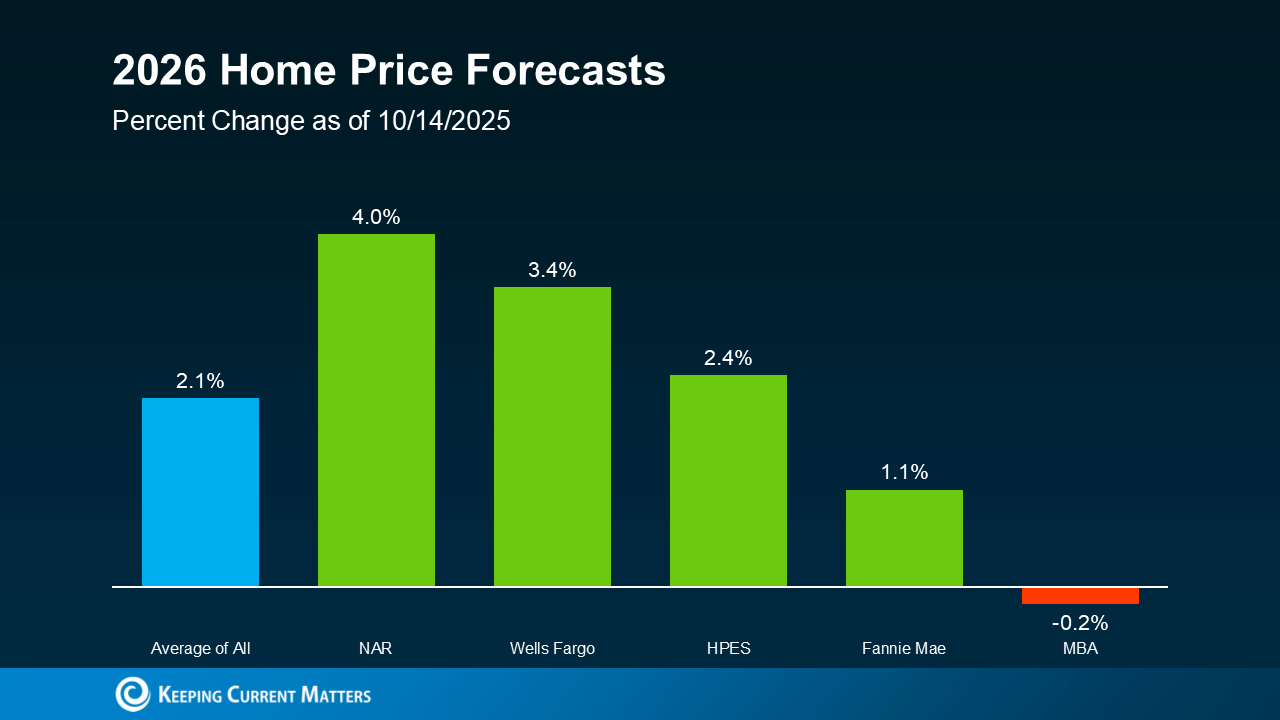

How are home prices behaving in 2026?

Home prices increased in 71% of metro areas during the first quarter of 2026, though the pace of appreciation is normalizing. The national median single-family home price reached $404,300 in early 2026, a modest 0.5% increase year-over-year. This cooling of price growth is a welcome signal for buyers, suggesting that while values are not crashing, the era of double-digit bidding wars has largely transitioned into a more balanced negotiation phase in 167 out of 235 tracked markets.

Regional Price Trends Comparison

Market Segment | 2026 Q1 Price Movement | Impact on Buyer Strategy |

|---|---|---|

Growth Markets | Prices up 3% or more in select Sunbelt and Tech hubs. | Requires rapid offer submission and pre-approved DPA readiness. |

Stable Markets | Prices hovering within 0.5% of 2025 levels. | Allows for traditional inspection periods and more seller concessions. |

Correction Markets | Slight declines in 29% of metros after 2024-25 peaks. | Potential for value-investing and negotiating on property repairs. |

What assistance is available for first-time buyers?

As of April 2026, there are 2,679 homebuyer assistance programs nationwide, a significant increase designed to combat persistent affordability gaps. These programs are no longer niche offerings; roughly 77% are actively funded and provide an average benefit of approximately $18,000 to help with down payments and closing costs. For the average 2026 first-time buyer—who is typically 38 years old with a $97,000 household income—these grants are often the deciding factor in qualifying for a loan.

Common 2026 Assistance Tiers:

MassHousing Grants: Eligible buyers can secure up to $25,000 in 0% interest assistance, potentially saving $31,000 over the loan's life.

FHA Specialized Programs: Various state-level FHA partners offer forgiven or deferred second mortgages to cover the 3.5% down payment requirement.

Local Municipal Grants: Cities like Springfield are currently accepting applications for $10,000 to $20,000 grants specifically for those looking to close in mid-2026.

How does Federal Reserve policy impact your mortgage?

The Federal Reserve’s June 2026 FOMC projections signal a "stable-to-lower" trajectory for interest rates, which has effectively set a floor for mortgage pricing. While the Fed does not set mortgage rates directly, their management of the federal funds rate influences the 10-year Treasury yield, to which most 30-year fixed mortgages are pegged. With inflation nearing target levels, the June 26, 2026 interest rate data suggests that lenders have sufficient capital to maintain competitive pricing, as confirmed by latest annual bank stress tests.

How is housing inventory impacting the 2026 market?

Housing inventory in 2026 is projected to increase by roughly 20% year-over-year, finally providing the structural relief required to temper rapid price appreciation. This surge is not merely a result of new construction; it is the byproduct of the "unfreezing" of the existing-home market. For years, homeowners carrying 3% mortgage rates were incentivized to stay put, but as life events—retirements, job changes, and family growth—accumulated, the pressure to move has finally outweighed the desire to retain a legacy interest rate.

The increase in supply is particularly visible in the suburban "ring" markets surrounding major metro areas. While urban cores in cities like San Francisco and New York remain supply-constrained, mid-sized cities in the Southeast and Midwest are seeing a faster return to "normal" inventory levels, often reaching a four-to-five month supply. For sellers, this means a shift in strategy: homes must now be move-in ready and priced precisely to local benchmarks, as buyers no longer feel the desperate pressure to overlook major property flaws.

What economic indicators should buyers watch in mid-2026?

The primary economic indicator for 2026 real estate is the 10-year Treasury yield, which acts as the leading benchmark for long-term mortgage pricing. Throughout the first half of 2026, the spread between the 10-year Treasury and the 30-year fixed mortgage has remained slightly wider than historical averages, suggesting that while rates have stabilized, there is still room for downward compression if banking sector volatility remains low.

Prospective homeowners should also monitor the Consumer Price Index (CPI) readings closely. The Federal Reserve's stance on interest rates remains tethered to core inflation staying near the 2% target. As long as inflation prints remain in the "comfort zone," the risk of a late-2026 rate hike is minimal, providing a predictable environment for those looking to lock in construction loans or long-term financing.

Strategy for 2026 Market Participants

For Move-Up Buyers: Focus on the equity built over the 2021-2025 period. Many homeowners are sitting on record levels of home equity that can be leveraged to secure a significant down payment on a new property, often bypassing the need for high-LTV (loan-to-value) financing.

For First-Time Buyers: Prioritize modern grants over traditional savings. With over 2,600 active programs now in operation, your ability to secure a "silent second" mortgage or a forgivable grant is higher than at any point in the last decade.

For Investors: Localize your search to metros with sub-0.5% price growth. These "correction" or "stabilization" zones offer the best yield potential as rental demand remains high while entry costs have flattened.

The interplay between macroeconomic policy and local inventory makes 2026 a watershed year for the industry. While the national narrative suggests a comeback, the real wins are being found by individuals who understand how to navigate the intricate web of state-funded grants and Fed-driven rate windows.

FAQ: Navigating the 2026 Landscape

Can I get assistance if I have owned a home before?

Yes. Under the 2026 HUD definition, anyone who has not owned a primary residence in the last three years qualifies as a "first-time buyer" for most federal and many state assistance programs.

Are down payment assistance programs still funded in mid-2026?

The majority remain robust. Q1 2026 data shows that 2,073 programs (77%) are currently active and funded. However, some local programs, like those in Massachusetts, have specific windows (April to July 2026) for locking into increased $25,000 grant amounts.

What is the average household income needed to buy in 2026?

While it varies by region, the average first-time buyer in 2026 earns roughly $97,000. Buyers with lower incomes frequently bridge the gap using the record number of DPA programs now available to offset high monthly payments.

The 2026 real estate market represents a period of stabilization where inventory growth and financial assistance are finally meeting the demand of a new generation of buyers. For those navigating this landscape, success requires looking beyond the national headlines to secure local grants and time their moves with the Federal Reserve's stabilizing interest rate signals.

Discussion