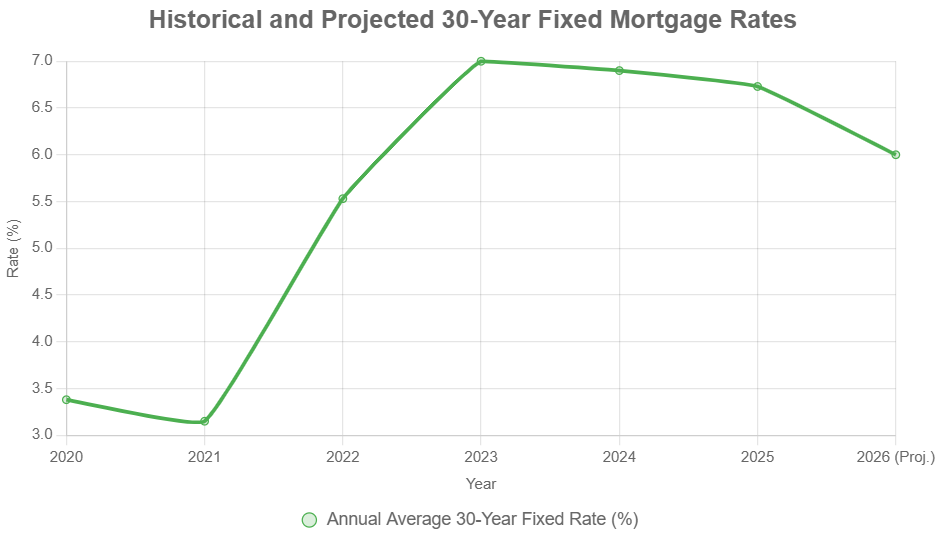

Buying a home in 2026 requires navigating a housing market that has finally begun to stabilize following years of post-pandemic volatility. With the 30-year fixed-rate mortgage averaging 6.47% as of June 2026, prospective buyers are seeing more predictable borrowing costs, though inventory remains a significant hurdle. Understanding the interplay between Federal Reserve policy, new credit reporting standards, and loan-specific requirements is now the baseline for any successful real estate transaction.

The current environment is defined by a "higher-for-longer" interest rate plateau that has reset consumer expectations. While the days of 3% rates are firmly in the past, the current mid-6% range represents a significant improvement from the peaks of previous years, providing a window for buyers who have been sidelined by extreme affordability constraints.

How do Federal Reserve projections impact your 2026 mortgage rate?

The Federal Reserve’s June 17, 2026, economic projections indicate a steady policy rate as inflation continues its gradual descent toward the 2% target. For mortgage borrowers, this stabilization means that the "scare factor" of rapidly rising rates has largely dissipated, allowing for more confident long-term financial planning.

Mortgage rates do not move in lockstep with the Fed funds rate, but they are heavily influenced by the 10-year Treasury yield, which responds to the Fed’s inflation outlook. In 2026, the Federal Reserve has maintained a focus on balancing labor market strength with price stability. As Core PCE inflation shows signs of anchoring, the risk of unexpected upward spikes in mortgage interest has diminished. This predictability is vital for lenders, who are now more willing to offer competitive spreads over benchmark yields.

What are the updated credit score requirements for 2026?

A major shift in mortgage underwriting for 2026 is the inclusion of "alternative data" such as utility and rental payment history in credit profiles. While the traditional FICO score of 620 remains the baseline for most conventional loans, lenders are increasingly leveraging these expanded profiles to approve borrowers who may have had "thin" credit files in the past.

These changes primarily benefit first-time homebuyers and younger adults who have consistently paid rent but lacked traditional credit accounts like car loans or credit cards. By 2026, major capital providers in the mortgage market have removed strict 620 minimums for certain programs, opting instead for a holistic view of financial responsibility. However, a higher score still translates directly to lower monthly payments: a borrower with a 740 score might secure a rate 0.5% to 0.75% lower than one with a 640 score.

Comparing common 2026 mortgage loan programs

Borrowers in 2026 have several distinct paths to homeownership, each with specific trade-offs regarding down payments, insurance, and eligibility. Most buyers still gravitate toward conventional loans, but government-backed programs remain essential for those with lower cash reserves or unique service backgrounds.

Feature | Conventional Loan | FHA Loan | VA Loan |

|---|---|---|---|

Minimum Down Payment | 3% for first-time buyers, 5% for repeat buyers. | 3.5% with a 580+ score; 10% for scores 500–579. | 0% down for eligible veterans and active service. |

Credit Score Goal | 620 is standard, but 740+ earns the best market rates. | 580 is the typical threshold for the lowest down payment. | No statutory minimum, but lenders often require 580–620. |

Why it Matters | Offers the most flexibility and allows for private mortgage insurance (PMI) removal later. | Essential for buyers with lower credit scores or limited savings. | The most affordable entry point for those who have served in the military. |

Why is debt-to-income (DTI) ratio critical in this market?

As of 2026, lenders are scrutinizing debt-to-income (DTI) ratios more closely than ever due to the elevated cost of living. Your DTI represents the percentage of your gross monthly income that goes toward paying debts. In the current lending environment, most conventional programs cap DTI at 50%, provided the borrower has "compensating factors" such as significant cash reserves or a high credit score.

For most borrowers, a "back-end" DTI of 36% to 43% is the target for a smooth approval. If your DTI exceeds these levels, lenders may require "PITIA reserves"—cash on hand to cover several months of Principal, Interest, Taxes, Insurance, and Association dues. In 2026, having three to six months of reserves is often the difference between an approval and a denial for those at the edge of affordability.

How to optimize your application for a 2026 mortgage

Preparation for a mortgage application now starts 12 to 18 months before the house hunt. With interest rates averaging 6.47%, every point of credit score movement can save a borrower tens of thousands of dollars over the life of a 30-year loan. Prospective buyers should focus on three specific areas to maximize their leverage.

First, minimize revolving debt. Carrying high balances on credit cards not only hurts your credit score but also inflates your DTI. Second, ensure all rental and utility payments are made through trackable bank transfers or official portals to take advantage of the new 2026 credit reporting standards. Finally, secure a pre-approval from a lender who uses the most current Fannie Mae or Freddie Mac underwriting engines. A pre-approval in 2026 is more than a price check; it is a signal to sellers that your financial profile has already been vetted against today's stricter criteria.

How do property tax assessments affect 2026 monthly payments?

While mortgage interest rates often dominate the headlines, the property tax component of a monthly payment has become a secondary "interest rate" for many 2026 homeowners. Property tax assessments are lagging indicators of home value growth, and in 2026, many jurisdictions are seeing significant "catch-up" increases that can add hundreds of dollars to an escrow account.

Homebuyers in 2026 must look beyond the purchase price and the current tax bill listed on real estate sites. Most counties reassess properties at the point of sale, meaning a home that was last sold in 2018 may have a tax bill based on a value that is 40% lower than the 2026 market price. This "reassessment shock" can push a borrower’s debt-to-income ratio over the limit during the underwriting process if the lender uses the anticipated new tax amount rather than the seller’s current bill.

Reliable 2026 estimates suggest that buyers should budget for property taxes at approximately 1.1% to 2.5% of the market value, depending on the state. High-tax states like New Jersey or Illinois require even deeper scrutiny of local millage rates. When calculating affordability, it is essential to ask your loan officer for a "fully loaded" payment estimate that includes the 2026 assessment projections, homeowners association (HOA) fees, and the rising costs of private insurance premiums.

The role of private mortgage insurance (PMI) in a mid-rate market

For 2026 buyers who cannot reach the traditional 20% down payment threshold, Private Mortgage Insurance (PMI) is a necessary tool that adds roughly $30 to $70 per month for every $100,000 borrowed. Unlike FHA mortgage insurance premiums, which typically last for the life of the loan, conventional PMI allows for removal once the borrower reaches 20% equity in the property.

In a market where home appreciation has slowed to a sustainable 3-4% annually, the "natural" path to removing PMI through value growth takes longer than it did in the early 2020s. Borrowers in 2026 are increasingly choosing "lender-paid PMI" or single-premium buyouts at closing. By paying a one-time fee upfront, a buyer can lower their permanent monthly overhead, which can be a strategic move if they plan to stay in the home for more than seven years.

Underwriting for PMI in 2026 also rewards higher credit scores. A borrower with a 760 score may see PMI rates that are less than half of what a 660-score borrower would pay. This reinforces the necessity of credit optimization before applying; a small bump in your score doesn't just lower your interest rate—it slashes your insurance costs.

Evaluating the "Buy Now, Refinance Later" strategy in 2026

The mantra of "marry the house, date the rate" has evolved into a more cautious financial strategy by mid-2026. While the possibility of future rate cuts exists, the Federal Reserve’s June 2026 stance suggests that the era of extreme low rates is not returning in the foreseeable future. Borrowers should never buy a home they cannot afford at today’s rates under the assumption of a guaranteed refinance window.

A smart 2026 refinement of this strategy involves looking at "recasting" as an alternative to a full refinance. Many conventional lenders now allow borrowers to make a large principal payment and then "recast" the remaining balance into a lower monthly payment without changing the original interest rate or paying new closing costs. This is particularly useful for 2026 buyers who may be selling a previous home after closing on their new one or who expect a significant liquidity event like a bonus or inheritance.

Refinancing remains a viable option if market rates drop by at least 0.75% to 1% below your current note. However, with average closing costs for a refinance hovering between 2% and 5% of the loan amount, the "break-even" point in 2026 typically requires at least 24 to 36 months of occupancy at the lower rate. If you plan to move sooner, the upfront costs of a refinance will likely outweigh the monthly interest savings.

Frequently Asked Questions

Can I buy a home with a 600 credit score in 2026?

Yes, you can qualify for an FHA loan with a credit score as low as 580 while putting down just 3.5%. Conventional loans generally require a 620, but the new inclusion of rental history in credit profiles may help those near the threshold bridge the gap.

Why is the 30-year fixed rate still above 6%?

While the Federal Reserve has stabilized rates, investors still require a premium to account for long-term inflation risks and market liquidity. Freddie Mac reports average rates of 6.47% as of June 2026, reflecting a resilient economy where demand for capital remains high.

How much should I save for a down payment in 2026?

While 20% is the traditional recommendation to avoid mortgage insurance, first-time buyers can qualify with as little as 3% for conventional loans or 3.5% for FHA loans. Veterans should utilize VA loans, which often require 0% down.

Is it better to wait for rates to drop further?

Attempting to "time" the market is risky. The Federal Reserve's current stance is a plateau rather than a steep decline. Waiting for a 1% drop in rates could result in higher home prices as more buyers enter the market, potentially offsetting any interest savings.

What documents do I need for a modern mortgage application?

In addition to the standard two years of W2s and tax returns, you should be prepared to provide proof of consistent rental payments and utility bills to benefit from contemporary credit reporting models. Lenders also require your most recent 60 days of bank statements for all asset accounts.

The 2026 mortgage landscape is one of balance. While the environment is more challenging than the record-low rate era, the increased transparency in credit reporting and the stabilization of Federal Reserve policy have created a sustainable foundation for long-term homeownership. Success in this market is not about finding a loophole, but about meticulous preparation and a clear understanding of the math behind the modern mortgage.

Discussion